The Positioning — Newsflash #4

- Merv Giam

- Mar 18

- 5 min read

Three portfolios. Same starting positions. Different decisions. Real money logic.

Week 4 · 6–12 March 2026

Editor’s note: This newsflash covers the week ending 12 March 2026. The following day, NST dropped 18% in a single session — a development covered in full in Newsflash #5. I’m publishing this issue as written because the decisions documented here deserve to stand on their own record. This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

All three portfolios are green. All three moved up this week. And yet the story isn’t as clean as those numbers suggest.

Last week I held the lead for the first time — the Strategist ahead of the Benchmark by six basis points. I wrote that one bad afternoon could erase it. It didn’t take an afternoon. The Benchmark retook the lead quietly, without a single trade, while I was busy dismissing alerts and adding to a position that was already overweight.

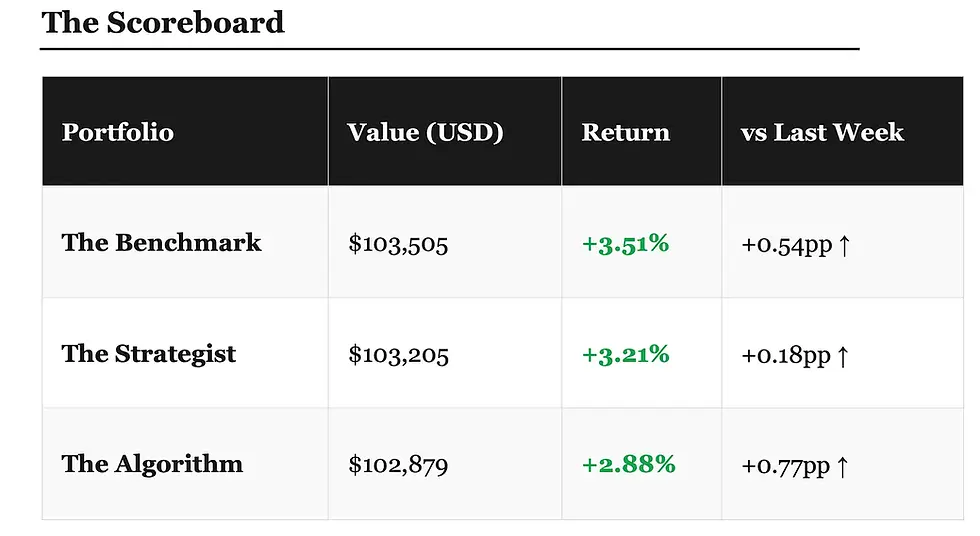

Four weeks in. The passive portfolio is winning. Again.

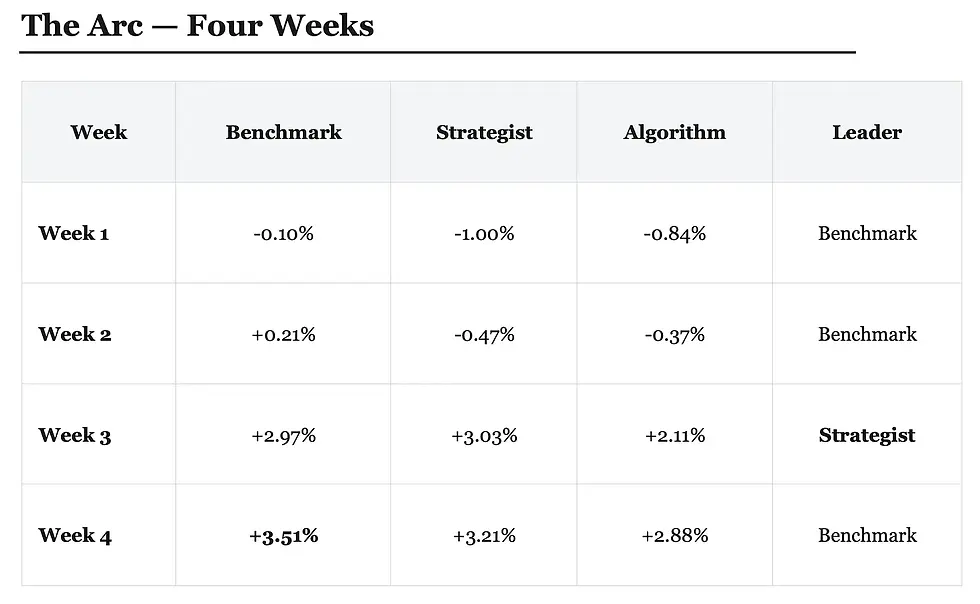

The Strategist led for exactly one week. The Benchmark has led for three. The Algorithm has never led. That’s the honest four-week picture.

What Happened This Week

Markets were choppy in both directions — up one day, down the next, with US and Australian markets moving in near lockstep, both driven almost entirely by global events rather than local fundamentals. Tariff headlines one day, de-escalation signals the next. The kind of week where conviction gets rewarded and second-guessing gets punished.

Two positions had genuine positive news. TLX and CU6 both received material product updates during the week — company-specific catalysts that moved both stocks independently of the broader noise. In a week where most of the market was at the mercy of macro headlines, having positions with their own positive story was the right place to be.

Gold is doing exactly what the thesis said it would. The debasement trade isn’t a future event — it’s happening in the data right now. Rate cut expectations have been pushed further out. Inflation is proving stickier than central banks projected. Hard assets are carrying portfolios that would otherwise be flat or negative on their US tech exposure.

The Strategist — My Week

One trade. One decision that actually required thought.

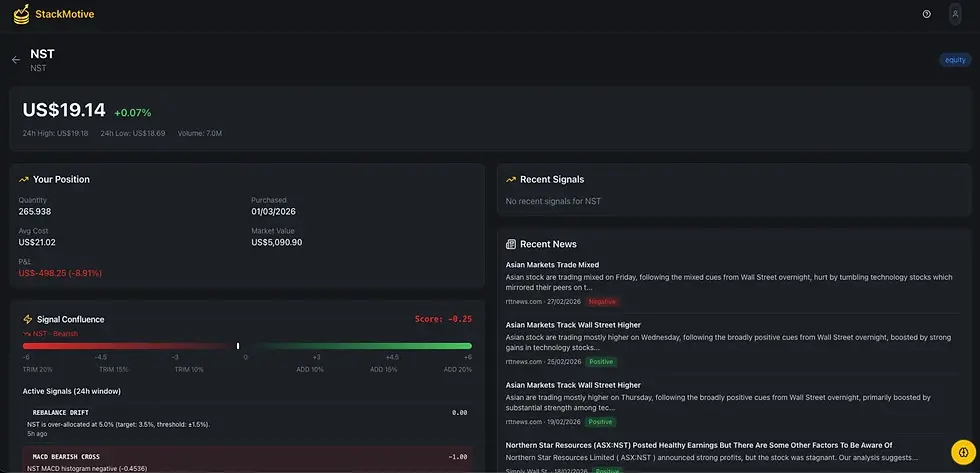

NST — ADD 53 shares @ A$25.31 (9 March) NST hit my pre-set DCA trigger at -12% from my average cost. The strategy rule was clear: at -12%, add. So I added — 53 shares at A$25.31, funded from existing cash. No agonising, no second-guessing. The rule existed for exactly this situation.

What I didn’t know when I bought was that NST was about to test whether that rule was right. On Friday 13 March, the day after this newsflash was due to publish — NST dropped 18% in a single session after releasing an operational update disclosing KCGM mill performance problems and a guidance cut. The position I added to on Monday on a clean rules-based signal was sitting at -26% from my average cost by Friday’s close. I’m covering this in full in Newsflash #5. But I’m flagging it here because the NST add is documented in this issue and you deserve to know what happened next.

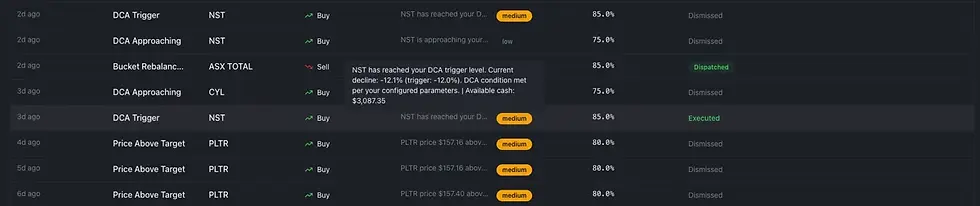

Everything else this week was dismissals. PLTR fired a watchlist price target alert six times in rapid succession on Sunday 8 March — I dismissed all six. CYL fired DCA approaching alerts across three separate days — dismissed each time. NST then fired multiple additional DCA and rebalance alerts after my buy, which I dismissed because NST was already above my target allocation after the purchase.

That last point is worth sitting with. I bought NST on Monday because the DCA rule triggered. By Thursday the system was flagging NST as 1.57% overweight — sitting at 5.07% of portfolio against a 3.5% target. The same position I just added to is now asking to be trimmed.

The system isn’t wrong. NST is overweight. But it has no memory of why it got there. It doesn’t know that I bought on Monday because a different rule told me to. It just sees a drift and flags it. That’s a real limitation of systematic signals applied without context — and it’s one the Algorithm has to live with every single day, with no human in the loop to resolve the contradiction.

The Algorithm — A Confession

Zero trades. Not one execution across the entire week. And I owe you an honest explanation for why.

When I reviewed the platform logs this week I discovered that auto-execution had been inadvertently disabled on 23 February — removed during a compliance review of the codebase. The Algorithm has been passive since then. Three weeks of Newsflashes described it as fully automated when it wasn’t. That’s on me for not catching it sooner.

It’s been fixed. Auto-execution is live again as of today. From this point forward, when a signal fires and the Algorithm’s criteria are met, it will execute without any human intervention — exactly as it was designed to.

What this means for the experiment: the last three weeks of Algorithm performance reflects a passive buy-and-hold approach, not an automated one. The Benchmark and the Algorithm have effectively been running the same strategy since 23 February. The divergence between them — Benchmark at +3.51%, Algorithm at +2.88% — is now explained entirely by the trades the Algorithm made in its first three days before auto-execution was disabled.

The real experiment starts again now.

The Benchmark — Still Winning by Doing Nothing

No trades. No decisions. No alerts reviewed. The Benchmark simply held its positions and collected the week’s gains.

$103,505. Best performing portfolio for three of four weeks. The most boring portfolio is the best portfolio. I keep writing that sentence because it keeps being true.

The gap between Benchmark and Strategist is now $300. That’s four weeks of active management producing a $300 deficit versus doing nothing. Not catastrophic. Not vindicated either.

What I’m Watching

The macro environment is becoming the story. US and Australian markets are increasingly correlated — both responding to the same global signals, both moving on the same headlines. In that environment, stock selection matters less and macro positioning matters more. The debasement thesis — hard assets, resource exposure, non-USD positions — is the right posture for this environment. The portfolios reflect that, which is why all three are green despite the noise.

One position I’m watching closely heading into next week: CYL is sitting at -13.8%, just 1.2% from my pre-set DCA trigger at -15%. If the market gives us another down day, that trigger fires. I’ll have to decide in advance whether I execute it or dismiss it — because by the time the alert lands, the moment to think clearly has already passed. That’s a decision for the weekend, not the morning the alert fires.

CYL did hit the trigger the following week. And NST, the position I just added to, dropped 18% on Friday 13 March. The week I described as one where “conviction gets rewarded” ended with a sharp reminder that signals reduce risk, they don’t eliminate it. Newsflash #5 covers both.

But the question I can’t answer yet is whether active management adds anything beyond what the thesis itself provides. The Benchmark holds the same positions. It’s green for the same reasons. My one trade this week — and seventeen dismissals — didn’t change the outcome meaningfully.

Maybe that’s the honest answer after four weeks. The thesis is working. The management layer is still unproven.

The Positioning tracks model portfolios for educational purposes. This is not financial advice. I hold positions in everything discussed here. All figures in USD at current exchange rates. Do your own research.

Comments